The Fed still shouldn't hike

and weekend reading

")

My bold prediction of financial stress and Fed capitulation last week was…not correct.

The market is cocksure that the Fed will go 75 at the next meeting. August Fed Funds (FFQ2) settled today at 97.675 (2.325%) and are a clean representation of market expectations for the next meeting. For zero premium you can sell a put and buy a call on August Fed funds1 such that you lose money if the Fed hikes more than 100 bp and make money if the Fed hikes less than 50 bps. That seems wrong to me. The probability of a negative shock that halts or slows Fed hiking seems much higher than an unexpected increase in inflation or inflation expectations.

In any event, I don’t think you can buy risk, unless you are playing for a squeeze, until either the Fed gets dovish because of lower inflation data or the market has already priced a recession.

I’m no econometrician, but if the money supply matters (I’m using the Divisia M42) we are getting much lower inflation prints in the coming months.

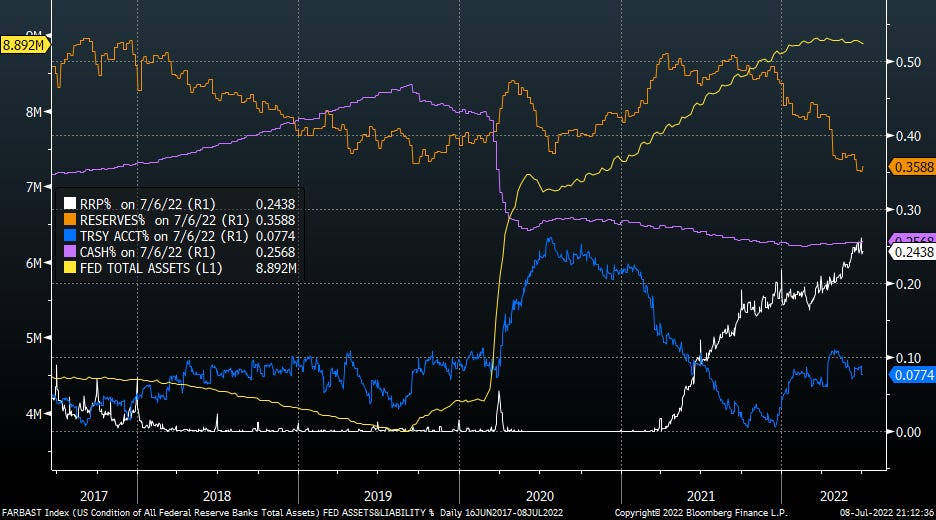

Can we learn anything from changes in the Fed’s liability mix? The only thing I find notable is that bank reserves continue to come down. If the banks needed or wanted more reserves to make loans they could easily raise deposit rates to bring funds back from the money markets. The banks aren’t doing that, which implies to me, that there isn’t inflationary loan demand.

Market monetarist take making the case that the if the Fed keeps NGPG growing at 5% (earlier this week a model had it at 4%), inflation will come off.

Richmond Fed paper about money market reform. 2020 showed that the 2014 reforms didn’t work for prime funds. Floating NAVs, liquidity buffers, and the ability to impose redemption fees and gates only encouraged earlier investor redemptions. The SEC is proposing new rules that would impose swing pricing, which tries to eliminate the incentive to redeem early, and increases the required daily and weekly liquidity. TBH, I don’t really see the point of money funds since we got rid of Reg Q caps on interest in the 1980s. The authors’ solution is to get the banks to backstop MMF liquidity contingently. That seems like a lazy way of putting the risk back into the banking system without having to address the G-SIB/LQR balance sheet challenge that banks already face in the Ample Reserve framework.

Manmohan Singh in the FT contra two recent papers saying every $1t of QT is equivalent to ~25 bps of tightening. Singh argues that the increased collateral availability from QT negates its implicit monetary tightening.

Russia, etc

Kaliningrad—I thought the European Commission had smoothed things over, but apparently not. Lithuania is quickly burning through any goodwill I still had from their 1992 Olympic basketball run.

Some movement towards sanity in the foreign policy establishment.

Ukraine’s leaders and its backers speak as if victory is just around the corner. But that view increasingly appears to be a fantasy. Ukraine and the West should therefore reconsider their ambitions and shift from a strategy of winning the war toward a more realistic approach: finding a diplomatic compromise that ends the fighting.

Bulgaria and North Macedonia—

Bulgaria’s pro-western government lost it’s parliamentary majority, ostensibly because it’s offer to support North Macedonia’s entry into the EU wasn’t pro-Bulgarian enough. The departing prime minister blames the Bulgarian mafia and Russia. Efforts to form a new government have failed and new elections are expected in September.

This being the Balkans, the Bulgarian support for North Macedonia’s EU ascension resulted in North Macedonian riots.

The EUR/BGN is pegged at ~1.956 in anticipation of joining the euro in 2024.

Bulgaria has a good debt sustainability profile, but it’s also very poor (~50% per capital GDP vs Europe).

The FX forwards are in line with short Eur rates, i.e. there is very little probability of a peg break priced

. It’s worth a look if you trade non g-7 fx.

Karakalpakstan—

Apparently, Karakalpakstan is part of Uzbekistan.

Recently the Uzbeks rug pulled Karakalpak a

utonomy.

Big protests and riots ensued.

My first thought was that this was either a CIA color revolution or Russia inspired unrest, but the evidence indicates it’s just garden variety ethno-political conflict.

Softbank

Rajiv Misra is leaving

My working theory is that Softbank’s insolvency will mark the bottom of this asset cycle, but I am doing a bunch more work before I jump to any conclusions—to be continued.

Miscellany

I’m not sure why I came across this now, it’s from 2014. But it’s like the Freedom Rock of levered blow-ups—turn it up man!

Hedge fund and bank trading disasters usually occur because traders overbet, the portfolio is not truly diversified and then trouble arises when a bad scenario occurs. We now discuss number of sensational failures including Metalgesllshart (1993), LTCM (1998), Niederhoffer (1997), Amaranth Advisors (2006), Merrill Lynch (2007), Société Genéralé (2008),Lehman (2008), AIG (2008), Citigroup (2008), MF Global (2012) and Monti Pashi (2013)

Correlation isn’t causation, but these charts, from a hard money/bitcoin enthusiast, are highly suggestive that closing the gold window wasn’t the best idea.

Yeah, I don’t think so. Also, why is the FBI making apps for the iPhone 4 now?

Sell FFQ2P 97.4375 (2.5625%) for 1/Buy FFQ2C 97.9375 (2.0625%) for 1. The breakevens are your strikes 2.5625 (Fed effective +98.25bps) and 2.0625 (Fed effective +48.25 bps)