Markets/Econ

Cliff Asness is jealous—Why Does Private Equity Get to Play Make-Believe With Prices?

Unlike Swensen’s PE market, which was primarily about earning extra return, today’s PE market is now seemingly as much about not having to report market prices.

related: Warren Buffett: Private Equity Firms Are Typically Very Dishonest

The overall figure for core inflation was 0.3% in January. Since housing is roughly 40%

a thirdof the core CPI, the 0.8% rise in shelter prices suggests that almost all of the 0.3% core inflation in December was caused by housing. The rest of the index barely changed.

The total size of the banking sector was little changed over 2022, but the static surface obscures a boom in lending of epic proportions. Banks changed the composition of their assets by replacing their cash and security holdings with loans to the real economy. Around $1.2t in loans were made in 2022, a level around three times higher than that of recent years. The same explosive growth is also seen in credit unions, which are functionally similar to small banks. Credit union loans outstanding grew $0.23t from 2021Q3 to 2022Q3 (Q4 data not available), a level also three times higher than recent years. Loan growth was strong across categories and appeared to persist despite rising rates.

Why inflation has declined but the economy remains healthy

Everything changed in late 2008, because that was when the Fed decided to pay interest on bank reserves and simultaneously adopted a policy of abundant reserves (aka Quantitative Easing). Money today is not scarce, bankruptcies are not exploding, yet inflation is coming down. Why? Because higher interest rates have served to balance the demand and the supply of money, and when that happens, inflation declines. Money in the bank pays 4% or so today, and that’s a lot more attractive than the 0% you could earn on money balances a year ago.

Current State of the Housing Market; Overview for mid-January

We are seeing a significant year-over-year decline in the housing market with fewer sales and more cancellations. We are just starting to see the impact on house prices. And even with a sharp decline in new listings, inventory is increasing YoY.

180 Million Barrels Of Crude May Never Be Returned to the Strategic Petroleum Reserve

A bigger problem, however, is whether the Department of Energy can afford to refill the SPR, as Wall Street Journal’s Jinjoo Lee suggested in a recent article. And the answer to this question may well be “No.”

Lee reports that the sale of 180 million barrels of crude from the SPR last year probably generated some $17.3 billion in proceeds at an average price of $96 per barrel. But of this $17.3 billion, $12.5 billion was set aside for use by Congress in the latest spending bill to fill the gap left by the cancellation of previously scheduled SPR sales for the period 2024 to 2027, according to ClearView Energy Partners.

This leaves the DoE with $4.8 billion to spend on replenishing the SPR, and, according to Lee, this could only buy 70 million barrels at WTI prices of $70 per barrel. This is less than half of what was released last year.

The Federal Reserve’s Balance Sheet: Costs to Taxpayers of Quantitative Easing

our analysis indicates that QE4 will cost taxpayers about $760 billion over a 10-year period. The Fed will absorb that cost by completely suspending its remittances to the US Treasury for the next five years and paying minimal remittances in subsequent years.

FTX Pre-Mortem Overview—SBF’s whiny substack where he blames my first employer, Sullivan & Cromwell, for being meanie heads and bullying him into filing FTX.

Over the course of 2021, Alameda’s Net Asset Value skyrocketed, to roughly $100b marked to market by the end of the year by my model. Even if you ignore assets like SRM that had much larger fully diluted than circulating supplies, I think it was still roughly $50b.

Man, if only he could’ve gotten his model to show a bid.

The special purpose acquisition company fallout is going to be spac-tacular

This merge-or-lose dilemma creates a significant potential conflict of interest, even if the shareholder right to redeem is an important protection. Some sponsors care about their reputation and prefer to swallow the loss over pushing a bad deal, but for others there is arguably an incentive to rush due diligence, underplay the risks, and overpay. Around 300 Spacs with $700bn in trust(opens a new window) have deadlines to invest in the first half of 2023, and the temptation is to throw a “Hail Mary(opens a new window)” pass and hope to score a deal in time.

As always, check out Jason Furman’s thread for a good detailed breakdown. Also check out his thread on alternate inflation measures. My favorite of these is median inflation, which measures what the price of the typical product in the economy is doing.

The Value of Corporate Pension Assets Fell Dramatically. Here’s Why That Doesn’t Matter

Here’s how it played out last year. Pension obligations fell by 26 percent in tandem with plan asset value, per WTW data. “It was a bit of a remarkable coincidence that both assets and liabilities fell by such a large but similar amount,” said Joe McDonald, senior partner at Aon, in a phone interview. Although 2022 may have been unkind to investment portfolios, it didn’t harm the health of corporate pension plans in the same way.

Retirements, Net Worth, and the Fall and Rise of Labor Force Participation

The increase in wealth during 2020 and 2021 plausibly contributed to the fall in labor force participation: As cited in a 2022 Economic Synopses essay, through September 2021, about 15% of the observed drop in LFP could be attributed to rising asset valuations; when we updated those calculations to include all of 2021, rising valuations accounted for about 20% of the drop. Even if changes in net worth were not the primary driver of retirements and labor force exits in the previous period, they certainly compounded them.

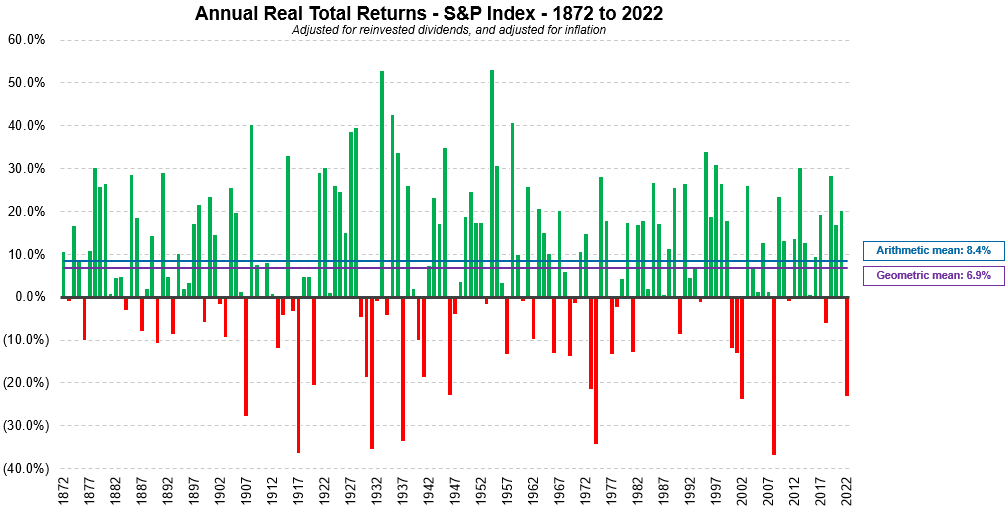

U.S. Stock Market Returns – a history from the 1870s to 2022

Miscellany

Why Britain’s (Severely) Underestimating British Collapse—Umair Haque needs to rest on his fainting couch.

This is the off-the-charts scale of British collapse. Like I said, it’s off the charts. That means that it’s singular. We literally have no comparisons for the sheer scale of what is happening in Britain. The greatest natural disasters in modern history don’t come close. The greatest terror attacks don’t approach it. British collapse — even on the simplest kinds of indicators, excess deaths — is like a supernova happening, something we have never seen before happen to a developed country. We simply have no reference point for it whatsoever. To call it a statistical outlier would be making a mockery of statistics.

U.S. Will No Longer Require Animal Testing for New Drugs

Previously, all drugs in development were required to undergo animal studies before being tested in human trials. Now, drug companies will still have the option to start testing experimental drugs on animals, but they won't have to.

600 year old spent nuclear fuel is just another poison

To answer that question, I need to draw your attention to a looming problem. Currently we have roughly 6.1 million tons of reasonably assured uranium reserves. If the planet were to be totally powered by nuclear using conventional reactors, these current reserves would last less than 5 years. While more uranium will be found, clearly this is not sustainable.

Fortunately, a solution exists: breeder reactors. Breeder reactors are not new. They go back to the dawn of the nuclear age. The Russians have had a 600 MW breeder operating since 1980 and an 800 MW breeder since 2016. China and India have active breeder programs. A breeder reactor can burn not only U-235 but also U-238. This will extend our uranium reserves by a factor of 140.

Then we would have at least 700 years before we need to dip into thorium and low grade uranium ores.

Right now in the USA alone, there is about 90,000 tons of already refined U-238 sitting in dry cask storage around the country. The stupidest thing we could do is put this fuel where we cannot get it. Of course, that's precisely what we are planning to do, in the form of deep geologic repositories, the equivalent of throwing diamonds into a volcano.

Wolfram|Alpha as the Way to Bring Computational Knowledge Superpowers to ChatGPT

It’s completely remarkable that a few-hundred-billion-parameter neural net that generates text a token at a time can do the kinds of things ChatGPT can. And given this dramatic—and unexpected—success, one might think that if one could just go on and “train a big enough network” one would be able to do absolutely anything with it. But it won’t work that way. Fundamental facts about computation—and notably the concept of computational irreducibility—make it clear it ultimately can’t. But what’s more relevant is what we’ve seen in the actual history of machine learning. There’ll be a big breakthrough (like ChatGPT). And improvement won’t stop. But what’s much more important is that there’ll be use cases found that are successful with what can be done, and that aren’t blocked by what can’t.