Weekend Reading

Markets/Econ

Cochrane on inflation—Waning inflation, supply and demand.

What happens next? In the simple fiscal theory model, the Fed can lower inflation today, but only by making future inflation a bit worse.

However, we have to inflate away debt at some point unless fiscal policy wakes up and decides to pay it back more aggressively. So we get more inflation in the long run. I call that "unpleasant interest rate arithmetic."

This leads me to worry about a 1975ish future:

Inflation goes down without dramatic Fed intervention, we all cheer, but then it gets stuck maybe around 4%. And we wait for the next shock, amid eerily 1970s arguments that we should get used to inflation, raise the inflation target, it's too costly to bring it down, or that it's really all about worker-manager conflicts of price gouging anyway.

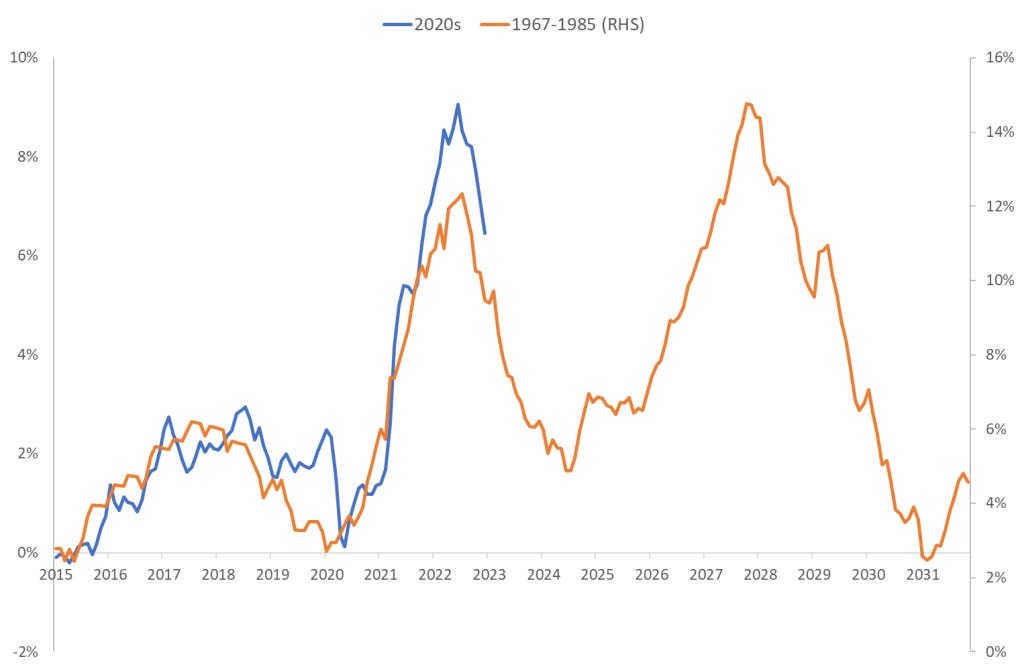

Striking similarities (and differences) between inflation today and in the 1970s

If the mistakes of the 1970s are repeated this time around, and inflation follows the same path as in the 1970s, the second round of inflation would be in 2026-2030, Figure 6 reveals.

My best guess, my hope you might say, is that this will not happen. I believe the Fed is concerned about its reputation after its failure to understand the persistence of post-pandemic inflation, meaning they will be keen to enforce their mandate. If this is correct, we should avoid a second-round peak in inflation.

Cochrane on the debt limit

Treasury secretary Janet Yellen should say out loud, right now "we pay principal and interest on treasury debt first, before anything else." President Biden should back her up. Drastic delays in social security, medicine, government shutdown and more are plenty enough threat to get Congress to move, without risking a run.

Zoltan in the FT—Great power conflict puts the dollar’s exorbitant privilege under threat. Btw, whatever you think about Zoltan, a wall street strategist having a mononym as a handle is remarkable.

Michael Pettis twitter thread contra Zoltan.

Retail sales may not be as bad as they look

As things get ‘back to normal,’ it’s reasonable to expect a decline in goods spending (or a slower increase) than in services spending.

We will know more next week about services spending—which is still most of total spending—in December. That will give us a better sense of how much the retail sales data signal overall weakness versus a relative shift from goods back to services. It’s likely to be some of both, but the split is informative for the likelihood of a recession.

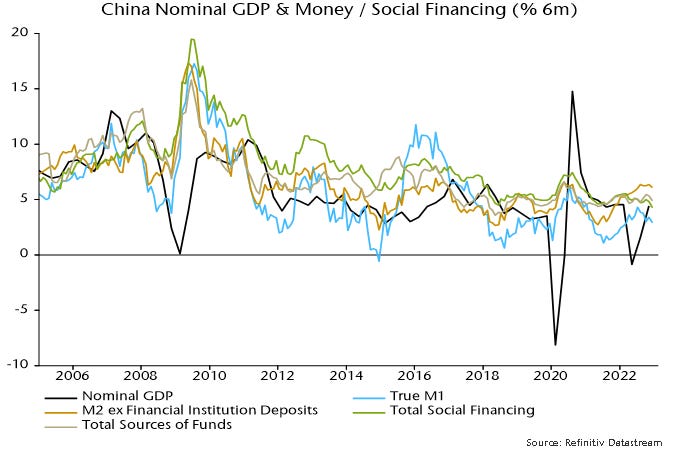

Money trends suggesting modest Chinese reopening boost

On reconsideration, Arthur Burns was still a bad Fed chair

Yes, oil shocks explain why inflation is higher one year than the next, but the Great Inflation of 1966-81 was caused by rapid NGDP growth, which was 100% due to the Fed printing too much money during a period when interest rates were not close to zero. I don’t see how this is even debatable.

Genesis has billions of dollars of debt, and the cryptocurrency industry no longer prints money (and perhaps never will again). Lenders tend to lend money to companies based on their ability to repay them, and that is something that Genesis (and Digital Currency Group) have proven repeatedly and publicly they are unable to do. Silbert himself got rich making bets on distressed assets, but I severely doubt any were as distressed as these.

So, the conclusion here appears to be that for the “dry powder” to be used, the most likely scenario would be one in which overall valuations fell (public and private market), creating an environment in which PE firms could continue to generate the IRRs that they want, consistent with the changed interest rate environment.

So the ostensibly bullish thesis of the hopeful investment bankers is dependent on a significant market correction. Short term pain, long term gain. When you put it like that, it’s not too implausible.

Except that . . . one of the things that is stopping prices from falling is the fact that in many cases they are supported by an expectation that there is a valuation floor under the market because of the likelihood of private equity bids for any company that looks cheap. After all, there is so much “dry powder” that has to be put to use etc etc …

The Recent Rise in Discount Window Borrowing

So far in 2022, small banks generally appear to have continued to rely on FHLB borrowing to meet funding needs, as their FHLB borrowing has risen by approximately 20 percent to $183 billion relative to the prior year, according to the most recently available Call Report data. But with the elimination of the DW primary credit rate penalty and the availability of term DW loans, it appears that DW credit has become more competitive with FHLB term advances. This is particularly true for longer dated maturities of sixteen to ninety days that comprise close to half of the DW primary credit loans outstanding in recent months, according to Federal Reserve data.

Foreign

Russo-Ukrainian War: The World Blood Pump

It is safe to say that western regime media has set a very low standard for reporting on the war in Ukraine, given the extent to which the mainstream narrative is disconnected from reality. Even given these low standards, the way the ongoing battle in Bakhmut is being presented to the population is truly ludicrous. The Bakhmut axis is being spun to western audiences as a perfect synthesis of all the tropes of Russian failure: in a nutshell, Russia is suffering horrible casualties as it struggles to capture a small town with negligible operational importance. British officials, in particular, have been highly vocal in recent weeks insisting that Bakhmut has little to no operational value.

The truth is the literal opposite of this story: Bakhmut is an operationally critical keystone position in the Ukrainian defense, and Russia has transformed it into a death pit which compels the Ukrainians to sacrifice exorbitant numbers of men in order to hold the position as long as possible. In fact, the insistence that Bakhmut is not operationally significant is mildly insulting to the audience, both because a quick glance at a map clearly shows it at the heart of the regional road network, and because Ukraine has thrown a huge number of units into the front there.

These positions are absolutely critical for Ukraine to hold. The loss of Bakhmut will mean the collapse of the last defensive line standing in the way of Slavyansk and Kramatorsk, which means Ukraine’s eastern position will rapidly contract to its fourth (and weakest) defensive belt.

…it does not appear that NATO wants to give Ukraine main battle tanks. At first it was suggested that tanks from storage could be dusted off and given to Kiev, but the manufacturer has stated that these vehicles are not in working order and would not be ready for combat until 2024. That leaves only the possibility of dipping directly into NATO’s own tank parks, which thus far they are reticent to do.

Why? My suggestion would simply be that NATO does not believe in Ukrainian victory. Ukraine cannot even dream of dislodging Russia from its position without an adequate tank force, and so the reticence to hand over tanks suggests that NATO thinks that this is only a dream anyway. Instead, they continue to prioritize weaponry that sustains Ukraine’s ability to fight a static defense (hence, the hundreds of artillery pieces) without indulging in flights of fancy about a great Ukrainian armored thrust into Crimea.

However, given the intense war fever that has built up in the west, it’s possible that political momentum imposes the choice upon us. It is possible that we have reached the point where the tail wags the dog, that NATO is trapped in its own rhetoric of unequivocal support until Ukraine wins a total victory, and we may yet see Leopard 2A4s burning on the steppe.

What if China decided to weaponize its dominance over this infrastructure, as Britain did in World War I? Such a campaign is likely to involve much more than ships stopping other ships. It could extend to denying access to Chinese-owned merchant ships, containers, ports, marine finance and insurance, cables, and satellites. In other words, it could target the virtual world of information and services alongside the physical world of ships and cargoes. The global economic damage caused by Russia’s chokehold over grain and energy flows pales in comparison to the upheaval that could result from the imagined scenario.

Peru’s crisis, years in the making, will not be easy to walk back. In the short term, it is hard to see how Boluarte and Congress, lacking broad-based legitimacy, can preside over anything more than continued democratic decline. In the long term, moving past the impasse will require constitutional reforms compelling both Congress and the executive to cede at least some of the powers they have routinely used to threaten the other. At this point, Congress can impeach a president for “permanent moral incapacity,” the vague grounds on which it tried and failed twice to boot Castillo from office. And the president needs only two votes of no confidence from legislators to shut Congress down.

Culture

Heretical thoughts on AI—What if AI changes everything except the economy?

What if AI ends up like the Internet—transformative to our daily lives while somehow not actually delivering major productivity gains? It’s worth considering.

Why are clinical trials so expensive? Tales from the beast’s belly

One cannot help but get the impression that this is an industry which is, at best, severely lacking in anything that could be called “human capital” and, in reality, simply deeply unserious.

More than two decades ago, Sen. Daniel Patrick Moynihan wrote that “the Cold War has bequeathed to us a vast secrecy system that shows no signs of receding.” What’s more, he continued, “it has become our characteristic mode of governance in the executive branch.” Keep in mind, he wrote this before the vast expansions of the secrecy bureaucracy following 9/11. The United States now has more secrets than ever—far more than it can possibly keep track of or justify on national security grounds. As of 2019, 4.2 million people in the United States held security clearances. That’s not a specialized core of security professionals; it’s the population of Los Angeles.

The Idiocy of America's Racial Classification System

The Asian American classification includes people with ancestry anywhere from Pakistan to the Philippines. Imagine the absurdity of university officials using “Asian American” as a singular “diversity” classification! It’s so internally diverse, and includes people who ancestors include around sixty percent of the world’s population. And while we don’t often think about it, the white classification is a government-invented pseudo-race, including everyone from Icelanders to Yemenis, people who don’t have anything more in common than do Filipinos and Pakistanis. Also, the Hispanic ethnic classification makes little sense—most Hispanics self-identify as “racially” white and often look European. Why do they, but no other “white” ethnicity, get a special category?

What's the real cost of CO2? The EPA relies on sloppy science in a new CO2 cost estimate

— The EPA’s estimates are extremely sensitive to discount rate changes.

— There’s a lot of uncertainty. The cost could even be near $0/ton, depending on one’s expectations for future tech. On the other hand, people may have their own non-economic reasons for going above the range — but the EPA’s proposed increase to $190 is based on sloppy science that is not justifiable.

Don't be miffed if you are mystified by the title. You're probably better off for it. LNT stands for Linear No Threshold. It's the hypothesis that radiation harm is strictly proportional to the dose no matter how rapidly or slowly that dose is received. This is like saying taking one aspirin a day for a year is the same as taking 365 aspirins in a day. LNT is the foundation for all our radiation regulation and response. LNT is nonsense.

Health

Semaglutide—Plaintiff’s attorneys—NB

…eventually these drugs will be withdrawn. So what will happen to folks with years of adipocyte hyperplasia, where individual cell hypertrophy has been suppressed? Their very numerous small adipocytes will, without their uncoupling drug, become enormous. People will become hungry as they develop hypertophy of all of those lovely tiny insulin sensitive adipocytes. Oops. It's gonnabe bad, but that's years down the road.