Weekend Reading

Markets/Econ

Chart #8 shows the year over year changes in the Personal Consumption Deflators (with the Core version being the Fed's favorite measure of inflation). Both rates came in a few tenths of a percent higher than the market expected. Does that sound like inflation accelerating? Or running hot? No. Inflation pressures peaked many months ago. Both of these measures are on track to show year over year gains that are much lower than their current level. It takes time for monetary policy–which is undoubtedly tight—to work its way through the economy. We just need to be patient.

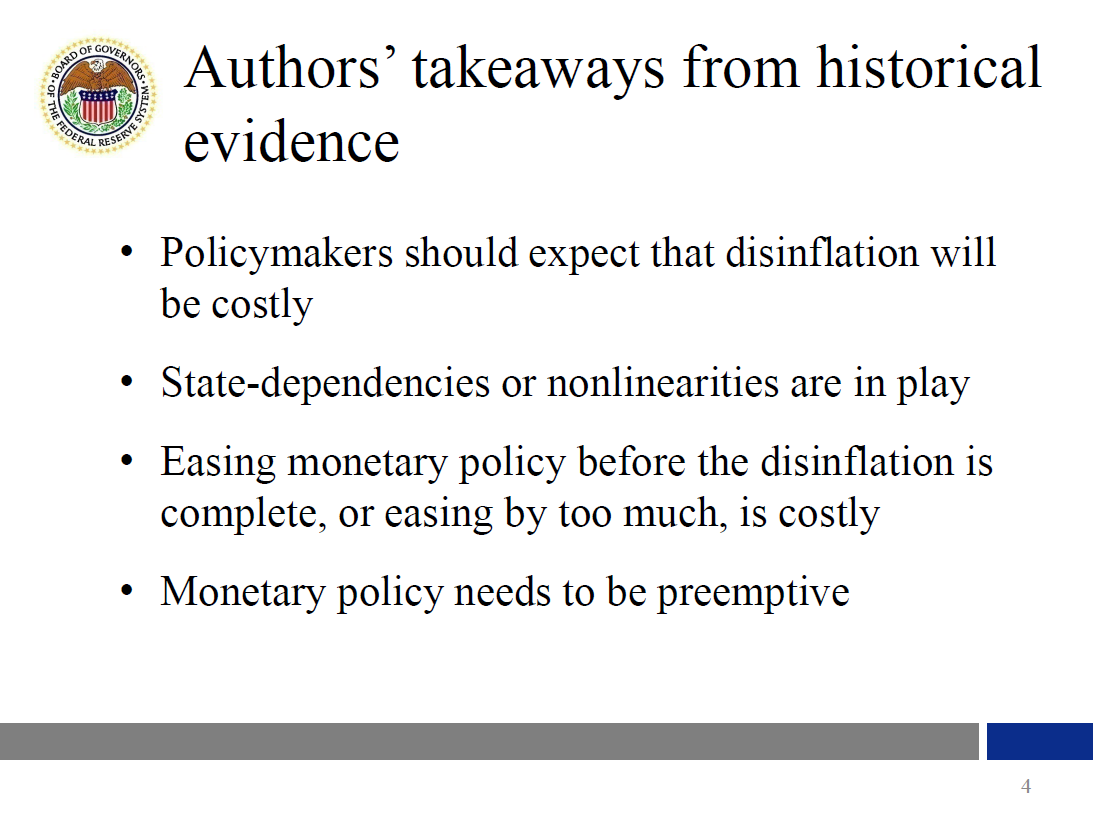

The authors' first takeaway, based on past disinflation episodes in the United States and abroad, is that policymakers should expect that disinflation will be costly in terms of foregone output or employment. They find that all 16 of the large policy-induced disinflations in the four advanced economies they study were associated with a recession.1

{kind=link}

The authors' second takeaway from history is that state dependencies or nonlinearities are also in play. The state dependency they note is that a higher initial inflation rate is associated with a lower sacrifice ratio. To explain this finding, they advance an argument based on policy credibility. Specifically, they argue that a high initial inflation rate enhances the plausibility of central banks' willingness to incur the cost of reducing inflation.

The authors' third takeaway from history is that easing monetary policy before the disinflation is complete, or easing by too much, is costly.5 My reading of this claim is that while central bankers might entertain hopes that they will directly see a dividend from early, forceful policy actions, historical experience suggests that they should not count on such a favorable outcome.

The “reality”, BofA argues, is “more nuanced”:

“(i) half of all SPX 0DTE option trades are “single-leg auto-execution”, a category uniquely skewed towards more ask volume early in the day but more bid volume later in the day (consistent with 0DTE buyers in the morning who then unwind as the day progresses); (ii) SPX 0DTE implied vol typically trades 10-15 vol points above longer-dated implies and with an embedded vol risk premium (VRP) 2.5x larger and likely inconsistent with a market overrun by option sellers; and (iii) history shows high payout ratios can frequently be achieved by directionally owning 0DTE “lottery tickets” despite paying elevated vol.”

Is It Time For a Holistic Review of Liquidity Requirements?

In 2005, liquid assets (defined as reserve balances, Treasury securities, agency debt, and agency MBS) were 10.6 percent of bank holding company assets. At the end of 2022, they were 23.6 percent. Because of the balance sheet constraints imposed by capital requirements, that increased share of liquid assets implies a reduced supply of loans to businesses and households.[15] Although some increase in holdings of liquid assets relative to pre-GFC levels was surely warranted, it is far from clear that a more-than-doubling to a quarter of banks’ balance sheets is socially optimal. The BIS estimates that compliance with the NSFR alone has reduced GDP permanently by 8 basis points (LEI 2010) and that at current levels of capital, the social benefit is less than the social cost (see Nelson and Covas 2017). A BIS review of the literature reported findings that compliance with the LCR reduces the supply of bank credit by 3 to 6 percent.

Ironically, although the liquidity requirements were designed in part to reduce the likelihood that a bank would need to borrow from its central bank in the rare financial crisis, the result has been that banks rely on the Fed and the FHLBs (which have the implicit backing of the taxpayer) for liquidity all the time. Furthermore, the ability to cheaply stockpile reserves has meant that banks are not subject to the market discipline associated with maintaining access to money market funding.

Digital bonds – a new kid on the block

Siemens’ €60m, 1-year bond was issued on a public blockchain or digital ledger platform called Polygon…

It facilitates direct bond offerings to investors without the need for a traditional financial (‘TradFi’) institution or central clearing. Disintermediation benefits for issuers like Siemens include lower cost, higher transparency, and increased speed of execution and settlement. The absence of a ‘digital €’ however means that investment in Siemens’ new bond, and coupon payments, involves classic bank transfers for now, so not absolutely digital yet. The bond has a mechanism for peer-to-peer trades on Polygon. If the digital ledger is not operational for any reason, Siemens can switch the entire bond to another digital ledger, replace the digital bond with a traditional (‘analogue’) bond, or call the digital bond without bondholder consent.

How I imagine Debt Syndicate guys reacting —What the Hell is Wrong with You People - Office Space

Oil Fails To Gain Traction As Q1 Builds Continue

The oil market, for the time being, will remain concerned over the builds we are seeing in Q1. The most visible data, the US, will continue to weigh on sentiment until traders start to see draws return. But as we explained, the data in the coming weeks should start to change the sentiment.

We think there are still valid concerns like weak product demand and weak refining spreads, so we will need to see the reopening mobility data from China translate into higher oil demand before we can say we are fully out of the trenches for Q1.

THE WEEK THAT WAS IN FINANCIAL MARKETS – FEBRUARY 24

But here’s the thing. At the macro level, the federal government is a net payer of interest, which means that the Fed’s rate hikes work like expansionary fiscal policy in the sense that they translate into hundreds of billions of dollars in additional spending by the federal government. Here’s how Warren Mosler explains it in his MMT White Paper:

“MMT recognizes that a positive policy rate results in a payment of interest that can be understood as ‘basic income for those who already have money.’

MMT recognizes that with the government a net payer of interest, higher interest rates can impart an expansionary, inflationary (and regressive) bias through two types of channels -- interest income channels and forward pricing channels. This means that what’s called Fed ‘tightening’ by increasing rates may increase total spending and foster price increases, contrary to the advertised intended effects of reducing demand and bringing down inflation.

Likewise, lowering rates removes interest income from the economy which works to reduce demand and bring down inflation, again contrary to advertised intended effects.”

More details emerge in billionaire Thomas Lee's suicide

Can the Fed bring inflation down alone?

The Fed’s interest rate tools are best suited for demand-driven inflation.

Covid and the war in Ukraine caused supply-driven inflation.

Financial markets pass along the Fed’s rate but don’t always agree.

Household finances are good, so interest rates are affecting demand less.

It’s best to solve labor shortages with more workers than fewer customers.

Congress and the White House have tools to solve supply-driven inflation.

The job market for new grads: worse than in 2008, but better than 2002

Foreign

Still more misguided is the notion that the PLA or other regime hard-liners sought to sabotage Blinken’s visit to frustrate Xi’s interest in détente. Xi is a hard-liner. Watching the first two years of the Biden administration has affirmed his judgment that U.S. hostility to China is deeply bipartisan and that therefore the United States is China’s implacable enemy. After six years of a perceived de facto war launched and waged by Washington to deny Beijing its strategic ambitions and overthrow the CCP, spy balloons seem inoffensive in comparison. Xi probably does not see the balloon program as in conflict with wanting Blinken to visit.

Yet U.S. President Joe Biden and his top officials repeatedly demonstrate little awareness of these critical differences between the American and Chinese systems. Biden tells Xi he wants competition instead of conflict but then repeatedly says publicly that the United States will defend Taiwan militarily and quips in his State of the Union address that no foreign leader wants Xi’s job. His secretary of defense is mystified that his Chinese counterpart will not answer the phone, and Biden’s advisers wonder why China will not discuss security guardrails. The answer is that Xi does not want them

The West Lives On in the Taliban’s Afghanistan

“Nobody is going to hurt us, dude,” he said, curling his lips into a smile. “We’re not in San Francisco.”

The poor logistical capacity of the state has proven the most important limit on the Taliban’s ability to reshape Afghan life.

The cities were safe for a reason. After coming into power, the Taliban initiated a hard-edged campaign for public order which has yielded undeniable results. Their methods had been fierce. Not long after taking power, the Taliban had asked neighborhood elders for lists of known criminals; within a few weeks, they had killed all the consensus nominees.

“Martyrdom,” he said, “would make me much happier than being a bureaucrat and working in the ministry. On the word of Sirajuddin Haqqani, we would happily blow ourselves up tomorrow!”

Hearing his words, it was hard not to feel the sense that something had passed away. It was like listening to a cowboy reminiscence about the closing of the frontier. The Taliban had won their revolution, and had everything they’d ever wanted. But now they confronted the truth that all successful revolutions face: winning a state is a lot more glorious than managing one. To their new world—a world of responsibility, a world that demanded a different sort of synthesis—they seemed to have little in the way of an answer.

Munich conference as prelude to a wider war

Remembering the Munich “peace conference” of September 1938 and its consequences, one wonders if there’s something bad in the water in the Bavarian capital, but that’s another topic.

The fact is that at the famed Hotel Bayrischer Hof on February 18, US Vice President Kamala Harris was trotted out to declare that “The United States has formally determined that Russia has committed crimes against humanity.”

How and by whom exactly that determination was made, she didn’t say. But crimes against humanity cannot be dealt with in a negotiation.

I recently came across a story covering declassified intelligence cables sent by Canadian peacekeepers on the ground during the war in Bosnia. Working my way through the cables, I couldn’t help but be reminded of my own time there and think about what we see coming from Ukraine. Those at the helm of Leviathan may lack the subtlety and discretion of previous generations, but when it comes to stoking tensions into conflicts and conflicts into wars, they still remember all the old moves.

As was the case in Yugoslavia, Washington shows no interest in de-escalating the conflict. Similar to the way US and NATO sought to directly aid Serbian adversaries on the ground while applying political pressure in such a way that ”deliberately set the bar higher than the Serbs could accept,” they presented the dominant regional power with the choice of either capitulating or finding allies and cultivating a deeper level of ferocity.

US/Culture

Mamas don’t let your babies grow up to post selfies

Social Media is a Major Cause of the Mental Illness Epidemic in Teen Girls. Here’s the Evidence.

…social media creates a cohort effect: something that happened to a whole cohort of young people, including those who don’t use social media. It also creates a trap—a collective action problem—for girls and for parents. Each girl might be worse off quitting Instagram even though all girls would be better off if everyone quit.

An implication of this analysis is that the correlations we are about to look at probably underestimate the true effect of social media as a cause of the teen mental illness epidemic.

There is one giant, obvious, international, and gendered cause: Social media. Instagram was founded in 2010. The iPhone 4 was released then too—the first smartphone with a front-facing camera. In 2012 Facebook bought Instagram, and that’s the year that its user base exploded. By 2015, it was becoming normal for 12-year-old girls to spend hours each day taking selfies, editing selfies, and posting them for friends, enemies, and strangers to comment on, while also spending hours each day scrolling through photos of other girls and fabulously wealthy female celebrities with (seemingly) vastly superior bodies and lives. The hours girls spent each day on Instagram were taken from sleep, exercise, and time with friends and family. What did we think would happen to them?

The Collaborative Review doc that Jean Twenge, Zach Rausch and I have put together collects more than a hundred correlational, longitudinal, and experimental studies, on both sides of the question. Taken as a whole, it shows strong and clear evidence of causation, not just correlation. There are surely other contributing causes, but the Collaborative Review doc points strongly to this conclusion: Social Media is a Major Cause of the Mental Illness Epidemic in Teen Girls.

Restoring American Manufacturing: A Practical Guide

America’s soaring trade deficit, now running at a record $1.32 trillion annual rate, requires the United States to sell paper to its foreign suppliers in return for goods. Most of the paper the United States sold to foreigners during the past few years was equity in US corporations, rather than government or corporate bonds. Valuations in the US stock market soared as the Federal Reserve forced interest rates lower, by reducing its short-term lending rate to zero and by purchasing $6 trillion of Treasury securities.

What if foreigners stop buying US equities? Several things can happen (and all of them probably will). First, the United States will have to sell more bonds to foreigners, and at more attractive yields. That means real yields will have to rise even further, putting more pressure on equity valuations. Secondly, foreigners will cut the price at which they buy US assets—that is, the dollar will have to fall. Third, Americans will buy fewer foreign goods, which means that demand will fall. That’s another name for a recession.

But in 1956 at the opening of the Calder Hall plutonium production facility in the UK, a young Queen Elizabeth was invited to handle a lump of plutonium and feel the warmth of the extraordinary material, which she did.1 The shielding was a plastic bag and I presume the royal gloves. The Queen outlived almost all her contemporaries.

Jimmy Carter: Unlucky President, Lucky Man

Whatever his role, whatever the outside assessment of him, whether luck was running with him or against, Carter was the same. He was self-controlled and disciplined. He liked mordant, edgy humor. He was enormously intelligent—and aware of it—politically crafty, and deeply spiritual. And he was intelligent, crafty, and spiritual enough to recognize inevitable trade-offs between his ambitions and his ideals. People who knew him at one stage of his life would recognize him at another.

Jimmy Carter didn’t change. Luck and circumstances did.

Welcome to America’s Racialized Medical Schools

That ideology is exemplified by a research methodology called “public health critical race praxis” (PHCRP)—designed, as the name suggests, to apply critical race theory to the field of public health—which asserts that “the ubiquity of racism, not its absence, characterizes society’s normal state.” In practice, PHCRP involves embracing sweeping claims about the primacy of racialization, guided by statements like “socially constructed racial categories are the bases for ordering society.”

These race-first imperatives have now come to influence the research priorities of major institutions. Perhaps no better case study exists than that of the University of California, San Francisco (UCSF), an institution devoted exclusively to the medical sciences, and one of the top recipients of federal grants from the National Institutes of Health.

The blast furnace - 800 years of technology improvement

The modern world uses shocking amounts of steel - in the US, we make roughly 575 pounds of steel per person per year. At the peak of US steelmaking in the late 1960s, it was closer to 1500 pounds per person, which is roughly how much China makes now.

Modern steel is produced by two different methods. The first uses an electric arc furnace to melt recycled steel scrap. The second method is to make new steel out of iron ore. While new steel can also be made in an electric arc furnace via the direct reduction route, most new steel starts life in a blast furnace.

the metaphysics of Waffle House

Heaven is always open— 24/7, 365 days a year. Its relief may only be intimated in glimpses here on Earth, but you nevertheless anticipate it exists at a constant somewhere else in the distance. A place outside of time waiting for you in eternity. That is the promise of Christianity. And that is the promise of the American Waffle House.

The Waffle House represents the miracle of a forever-abundant Garden. Your cup of coffee runneth over— like magic it becomes filled before you can even finish it. A buzzy, Southern waitress takes your personally customized order and in minutes it is prepared and served for you. Her regional hospitality makes you and everyone feel welcome and attended to. The fantasy of both equality and individuality is achieved in a Heavenly balance, fulfilling the American dream “every man a king.”

I drove north toward Montana, where I visited with a man named Paul McNiel, whom I’d first met back during the fervid summer of 2020, at a Fourth of July picnic and anti-government rally headlined “Rage Against the State.” “I think that Livingston has the highest per-capita concentration of contributors to The New Yorker of any city in America,” he’d said when I introduced myself as a writer.

Jones himself had been visibly upset throughout the screening, getting up half a dozen times from his front-row seat to escape backstage. “I couldn’t watch myself through some of that,” he said during the Q&A. “I looked like Jabba the Hutt on PCP.”