good (GREAT!) Weekend Reading

2025 #16 (May 9)

Markets/Econ

Corporate share buybacks were a shock absorber in April’s sell-off

Macro utopia—Our first soft landing?

And so here we are. In March, 12-month PCE inflation was only 2.3%, not far above target. Unemployment has nudged up to 4.2%, but that’s still a relatively low level. It seems like we have a soft landing—the best macroeconomic outcome in American history. Of course almost no one feels that way. MAGA types believed the Biden economy was horrible, and Democrats fear that Trump is currently wrecking the economy.

The Fed also got lucky in a couple ways. Decades of relatively low inflation made younger workers forget the 1970s. The price spike of 2021-23 was viewed as being at least somewhat transitory, and thus wage inflation didn’t rise by quite as much as price inflation or NGDP growth. But another big factor was the immigration surge, which provided some badly needed additional labor when the economy was overheating due to excessive demand stimulus.

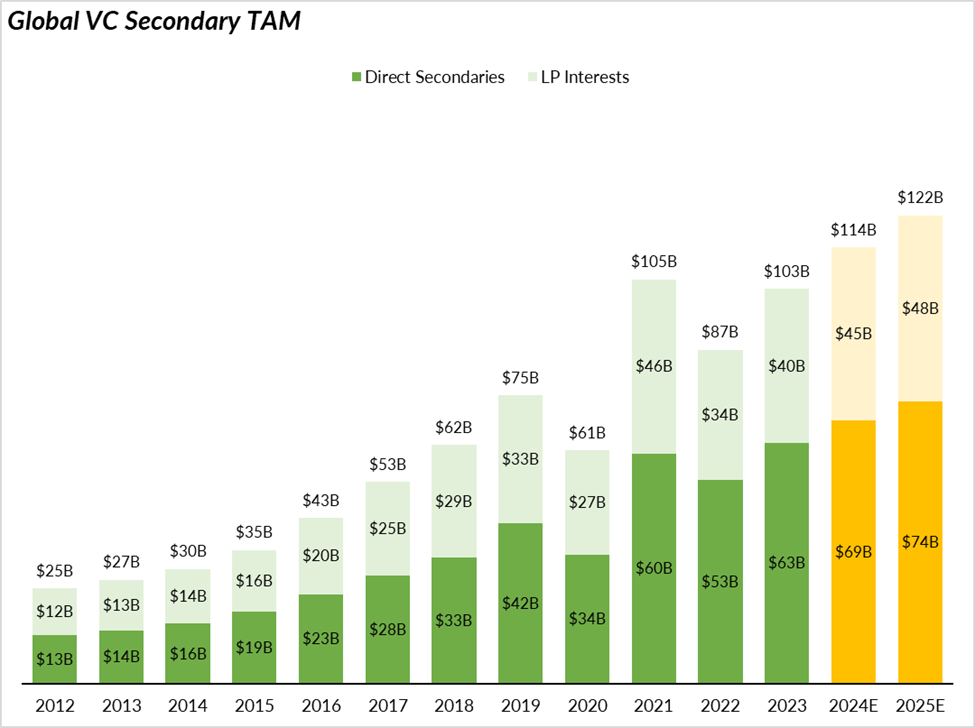

2023 – 2025E: How Big Is the Secondary Market for Venture Capital?

Why monetary policy should crack down harder during high inflation

Our findings suggest that central banks should adapt their approach to monetary policy during periods of high inflation. More aggressive policy measures can be implemented, taking advantage of the fact that the cost of reducing inflation is lower, in terms of lost output, when firms adjust their prices more frequently. However, as inflation decreases, monetary policy tightening becomes more costly again.

The Fed needs a "Strong" leader

One objection to this idea is that former chairs usually resign from the Board after their term as chair ends. But it doesn’t have to be that way. Under very unusual circumstances, a former chair might remain on the Board and continue providing leadership on the direction of policy. They would be especially likely to do so if their replacement were clearly unqualified.

This story caught my eye:

“Powell’s term as chair expires in May 2026. His underlying role as a governor continues through January 2028. Asked at Wednesday’s press conference whether he would also step down from the board when his chair term ends, he declined to answer.”

A shot across the bow?

What went wrong in the 1960s? There´s nothing wrong with the concept of potential real output, the guiding principle of policymakers in the sixties. The big problem is that it´s hard to estimate, especially in real time so that the chance that economic policy gets it wrong is high with the consequence that instead of higher real output the economy gets stranded with higher inflation.

Private equity’s best days are over, says Egyptian billionaire Nassef Sawiris

Private equity has seen its best days . . . They can’t exit. Exits are so tough,” Sawiris told the Financial Times.

“[Investors] are so frustrated. They are telling them [buyout firms]: ‘I haven’t seen any returns, you haven’t returned any cash to me in the last five, six years’.”

Sawiris took particular aim at the use of “continuation funds” to recycle capital — a tactic whereby private equity groups, instead of selling an asset to another owner or publicly listing it, move the asset into a new fund where they still maintain control.

“Continuation funds is the biggest scam ever because you say ‘I cannot sell the business, I’m going to lever it again’,” Sawiris said.

Doctors Warn Accountants of Private-Equity Drain on Quality: You Could Be Next

Kenneth Rogoff on Monetary Moves, Fiscal Gambits, and Classical Chess

I know that for years, people have said the US debt is unsustainable, but it hasn’t come to roost because we’ve lived through this post-financial crisis, post-pandemic era of very, very low and negative real interest rates. That is not the norm. There’s regression to mean.

You know what? It’s happened. Suddenly, the interest payments start piling up. I think they’ve at least doubled over the last few years. They’re quickly on their way to tripling, of going up to $1 trillion. Suddenly, it’s more than our defense spending. That’s the most important macro change in the world, that real interest rates appear to have regressed more towards long-term trend.

As the Fed continues its framework review, it faces a defining opportunity to upgrade its strategy for a world of more frequent supply shocks, volatile real-time data, and heightened political scrutiny. Anchoring policy to a nominal GDP path does not require abandoning the 2 percent inflation goal. Instead, it strengthens that commitment by embedding it within a broader and more resilient nominal anchor.

Should We Worry About Global Imbalances? On the significance of safe asset shortages

The challenge when it comes to safe assets is that we are not talking about a market with private sellers and private buyers. There is a basic friction in the market that prevents safe assets from being competitively supplied. The largest supplier of safe assets (by far) is the U.S. federal government. But the federal government is not deciding how much debt to issue based on the demand for safe assets (although they might respond to lower interest rates by borrowing more). Nonetheless, the market will clear. It is important to consider how the market clears and the corresponding welfare consequences.

There’s still ‘A Better Way’ (than tariffs). and The GOP Tax Bill Could Solve the Tariff Problem. Advocating for the destination based cash flow tax proposed in 2016.

Where does this leave us after the recent bounce and partial market retracement? The S&P 500’s forward multiple is 20x, and earnings are not properly reflecting recession risks. With a multiple of 20x, how much upside remains? In many recent crises—such as the 2002 double bottom, the 2011 European debt crisis, the 2015 emerging markets crisis, the 2018 trade war, and the 2022 rate hikes—the S&P 500’s multiple dropped to ~15, suggesting a ~20% decline from current levels. I have not yet heard a compelling argument why the multiple would not fall to ~15x and remain there for more than a few days during this crisis. Even assuming a quick earnings recovery to $300, a multiple of ~15x would place the S&P 500 below 5,000.

America’s Economic Tailwinds Will Override Trump and His Tariffs. Nouriel Roubini—USA A-OK

Platt’s long-term track record supports his bragging rights. Is he the best trader in the world ever? George Soros, Stanley Druckenmiller, Stevie Cohen, and others may have something to say about that.

What I find fascinating though is the sudden growth of multi-manager pod shops that have been around for decades but were small until now. Many of these don’t have the storied pedigree of being former heads of trading at Goldman Sachs or being CIOs at Citadel and Millennium. These include names like Hudson Bay Capital and Verition Fund Management. In 2018 the two firms were managing $2.5bn and $0.5bn respectively. Today, Hudson Bay Capital has $25-30bn and Verition has $12bn!

The Trillion-Dollar Private Credit Market Faces Its First Big Test

The International Monetary Fund reported last week that more than 40 percent of private credit borrowers had negative cash flow at the end of last year, “prolonging their reliance on payment-in-kind provisions and amend-and-extend restructurings.” And that was before the tariff wars roiled the markets.

The regulated banking system, however, isn’t immune to the potential problems of private credit. That’s because banks have lent more than $500 billion to private credit funds, according to the IMF. This credit extension is what is known as “back leverage.” It is leverage on top of leverage, allowing the funds to borrow at investment-grade levels from the banks and extend credit to their portfolio companies at much higher rates, profiting off the spread. The worrisome detail is that those portfolio companies have obtained leverage of five to ten times EBITDA, according to market participants.

Why the rich paid less tax in the 1970s – despite 98% tax rates

The lesson of the decades since the 1970s is that the best way to tax the wealthy is by expanding the base and closing loopholes. That makes a less snappy soundbite than sending rates sky-high, but the evidence and the history shows that it’s fairer and much more effective.

To see what Allbirds might have been, consider a rival “unsexy” shoe brand that has been racking up impressive sales — at higher price points than Allbirds’ — and attracting a passionately loyal following. And it’s doing it with a brand name that by rights should have belonged to Allbirds.

I don’t know why two Frenchmen chose a Māori name for their brand, but they were smart to do so. As a name, Hoka has several advantages over Allbirds:

—It’s easy to pronounce across multiple languages. The L and R sounds in the middle of Allbirds are notoriously difficult for speakers of many languages; “Allbirds” can be mis-heard as “Owlbirds” or “Auburns” or any number of other wrong choices.

—You don’t have to know what Hoka means; it just sounds fun and upbeat. It functions as an empty vessel, fillable with multiple meanings. That makes it suitable for brand expansion and extension.

—When you do know what Hoka means, it’s relevant and aspirational. You’re not walking or running — you’re flying!

—It even bears a sneaky resemblance to that other big four-letter sportswear brand with a K in third position: Nike.

Stripe accelerates the utility of AI and stablecoins with major launches

Foreign

How the Houthis Outlasted America

In short, although the U.S. campaign put the Houthis under tremendous pressure, they were far from deterred, much less defeated, at the time of the cease-fire. By early May, the United States was making tactical gains in destroying weapons and capabilities, pushing the leadership underground, and stirring up Houthi fears that a new ground campaign against them might soon be launched. But the United States was unable to turn these pressure points into strategic advantage.

Deep Rivalry or Elite Obsession? Washington’s Search for Dominance over China

The question Americans must ask is whether it is vitally important for their country to deny China this ambition. Must China remain subordinate in a system led by an unrivaled United States? Or can Americans live in a world that sees China and the United States as equals, as envisaged by Singaporean statesman Lee Kuan Yew?

To answer that question, American leaders will need to be much more open with their citizens about what is required to achieve dominance over China — a truly national effort over generations involving most arms of government and broader society. That’s what was needed to win the Cold War, and if this is indeed a new cold war, the challenge will be even greater.

China Is Still Winning the Battle for 5G—and 6G

Today, the United States and Europe—home of both Ericsson and Nokia—are sitting on a shrinking base, as China continues to undercut their sales pitches by subsidizing Huawei deployments around the world. Although Huawei’s global dominance in 5G has been slowed by U.S.-led sanctions and export controls, neither U.S. innovations nor those of its partners have threatened the competitiveness of its products. Given that Huawei’s research and development budget is more than twice the size of its two next-largest Western competitors, the company is unlikely to lose its innovation advantage.

China’s Tech Power is Overrated

China’s reputation as a tech powerhouse is built on selective and often misleading indicators. Impressive high-tech export figures are driven by foreign firms. Surging patent filings reflects bureaucratic manipulation. Billions in subsidies have failed to meaningfully boost productivity. And the broader economy is suffering from an acute “diffusion deficit”. Innovation is about more than just invention; it’s about embedding new technologies in a wide range of firms and industries.

The U.S.-Ukraine Agreement: Legality and Transparency

In this post, we explain why we believe that the agreement is likely a lawful “sole executive agreement” that the president need not submit to Congress and then analyze the relevance of recent reforms to the Case-Zablocki Act for the transparency of the agreement and an important related agreement that is being negotiated pursuant to it.

Drax is the greatest greenwashing scandal in Britain.

I have been fighting its destruction for years, not least because many of the trees come from near my home on the Cape Fear River in Carolina. I watch the cargo ships plying the wood, commencing a 4,000-mile trip to Yorkshire. It is beyond madness.

Drax claims to care about the environment, but its real motivation is money. Its CEO, Will Gardiner, paid himself £5million a year while his company has destroyed large swathes of forest. His company is a rapist of nature.

Ezra, Derek, and Dan Wang—Abundance and China

China is very messy. That is always my first proposition about China — it is very big, and many things are true about China all at the same time. They are a country that claims to be pursuing “socialism with Chinese characteristics,” which is still one of the most wonderful political science terms ever.

What sort of socialism is this? In my view, this is one of the most right-wing regimes in the world. A country that would make any American conservative salivate in terms of its immigration restrictions, its incredible amount of manufacturing prowess, and its enforcement of very traditional gender roles in which men have to be very macho and women have to bear children.

What’s Guiding Ukraine’s Deep Strikes? Something Putin Can’t Jam

Russia has constructed one of the most aggressive electronic warfare environments in the world. Near major cities, military bases, and strategic infrastructure, GPS signals are jammed, spoofed, or completely denied.

And yet Ukrainian drones continue to strike targets hundreds of kilometers inside Russian territory.

In some cases, they may be relying on inertial navigation, visual scene matching, or preloaded terrain maps. But the most adaptable—and scalable—solution is Signal-of-Opportunity Navigation.

Every FM tower in Belgorod. Every cell tower near an oil refinery in Tatarstan. Every civilian broadcast signal left untouched by Russian operators. These are not vulnerabilities in the traditional sense. They are fixed-position reference points, whether Moscow likes it or not.

USA Politics/Culture

"Managerial Bureaucracy’s Threat to Democracy and Humanity"

…this is an oligarchy of a uniquely modern kind, constituted by a very specific type of person. For ours is a managerial regime, a system of rule by managers. Today our ruling elites are drawn almost entirely from the professional managerial class, and that makes them a unique breed indeed. Because, fundamentally, the business of managers is not producing or building anything, providing any essential service, waging war, or even making any critical leadership decisions, but rather the constant manipulation and management — that is, surveillance and control — of people, information, money, and ideas.

To fully reclaim our true sovereignty — and our democratic liberty — we thus have no choice but to first recover our soul, and with it our courage and our humanity. And so, as Jünger wrote, in our frightened, managerial age, Man has been “initiated into his theological trial whether he realizes it or not.” Only by passing through this trial may we hope to emerge from mere functionality, to once more become Men with Chests. “Victory [over tyranny] comes when the assault of the ignoble is beaten back in one’s own breast,” Jünger proclaimed, and I believe this to be so. Only in victory in this battle can we hope to rise up from our fetal position as the Last Men at the end of History, cast off the heavy yoke of managerial oppression, and save humanity from ourselves.

We do not have much time left to solve this problem. US leaders are now warning that Chinese president Xi Jinping may seek to invade Taiwan by 2027, if not sooner. No matter how much more the United States spends on defense in the next few years, it will not result in a meaningful increase in our traditional military capabilities within this “window of maximum danger,” as Congressman Mike Gallagher has called it. We literally cannot build enough in time to matter.

If the goal is just to try to bully and intimidate federal judges into acquiescing in more unlawful activity by the Trump administration, that’s shameful enough. But suggesting that the President can unilaterally cut courts out of the loop solely because they’re disagreeing with him is suggesting that judicial review—indeed, that the Constitution itself—is just a convenience. Something tells me that even federal judges and justices who might otherwise be sympathetic to the government’s arguments on the merits in some of these cases will be troubled by the implication that their authority depends entirely upon the President’s beneficence.

The Epic Battle over the SEC's Surveillance System

The SEC’s name for this database is the Consolidated Audit Trail. The CAT, as it is more commonly referred to, has been one of the most contentious government initiatives in American history. There have been endless technical delays, turmoil over its oversight structure, and ever-shifting battles over funding. As one insider summarized to me via interview: “The CAT is a clusterfuck.”13 Nevertheless, it survived…bruised, battered, but never quite defeated. And the system is currently operational, allowing the SEC to monitor all U.S. equities and options trading.

In the late 2000s, Moldbug wrote some genuinely interesting speculations on novel sci-fi variants of autocracy. Admitting that the dictatorships of the 20th century were horrifying, he proposed creative ways to patch their vulnerabilities by combining 18th century monarchy with 22nd century cyberpunk to create something better than either. These ideas might not have been realistic. But they were cool, edgy, and had a certain intellectual appeal.

Then in the late 2010s, as soon as his ideas started getting close to power he dropped it all like a hot potato. The MAGA movement was exactly what 2000s Moldbug feared most - a cancerous outgrowth of democracy riding the same wave of populist anger as the 20th century dictatorships he loathed. But in the hope of winning a temporary political victory, he let them wear him as a skinsuit - giving their normal, boring autocratic tendencies the mystique of the cool, edgy, all-vulnerabilities-patched autocracy he foretold in his manifestos.

Competitive NYC: Value Proposition Tracker. We’re Number 1!

Science, Tech, and Health

Zvi Mowshowitz—Cheaters Gonna Cheat Cheat Cheat Cheat Cheat

Doing the assignments yourself is now optional unless you force the student to do it in front of you. Deal with it.

As for this being ‘grief and hassle’ for educators, yes, I am sure it is annoying when your system of forced fake work can be faked back at you more effectively and more often, and when there is a much better source of information and explanations available than you and your textbooks such that very little of what you are doing really has a point to it anymore.

and AI #115: The Evil Applications Division

Trump administration reiterates that it plans to change and simplify the export control rules on chips, and in particular to ease restrictions on the UAE, potentially during his visit next week. This is also mentioned:

“Stephanie Lai and Mackenzie Hawkins (Bloomberg): In the immediate term, though, the reprieve could be a boon to companies like Oracle Corp., which is planning a massive data center expansion in Malaysia that was set to blow past AI diffusion rule limits.”

If I found out the Malaysian data centers are not largely de facto Chinese data centers, I would be rather surprised. This is exactly the central case of why we need the new diffusion rules, or something with similar effects.

This is certainly one story you can tell about what is happening:

“Ian Sams: Two stories, same day, I’m sure totally unrelated…

NYT: UAE pours $2 billion into Trump crypto coins

Bloomberg: Trump White House may ease restrictions on selling AI chips to UAE.”

How the US Built 5,000 Ships in WWII

The commission acted like a trade association in its role as a distributor of information, but it was also the customer (and owner) of these shipyards, and it was a demanding one. The commission’s shipbuilding contracts rewarded yards for completing work ahead of schedule, and penalized them for falling behind. In extreme cases, the commission would replace a shipyard’s management if the existing team wasn’t meeting expectations. A Rhode Island shipyard operated by Rheem Manufacturing, for instance, was handed over to Henry Kaiser in 1943 when Rheem struggled to manage it.

All lines of evidence point to GLP-1RAs improving rather than worsening muscle quality and physical functioning. Though there is reason to be concerned about individuals who are at-risk for sarcopenia using the drugs when they should not, that is not an indictment of GLP-1RAs in general use or mechanistically.3 It is, instead, a point of caution doctors should keep in mind when making the choice to prescribe these drugs.

Is This the Man Who Created Covid-19 in Fauci’s US Lab?

It appears that Munster took Baric’s patented SARS virus-vaccine and made a transmissible version at his Rocky Mountain Lab (Baric’s version was not intended to be transmissible). What is the evidence for that? Perhaps most telling is that, as Haslam observes, SARS-CoV-2 transmits efficiently in only five known mammals, and those five – American deer, American deer mice, Syrian hamsters, American mink, and Egyptian fruit bats – are all found in Munster (and Fauci’s) Rocky Mountain Lab in Montana. SARS-CoV-2 doesn’t infect lab animals common in Chinese labs or present in the WIV, such as Chinese horseshoe bats. This would suggest that SARS-CoV-2 acquired its transmissibility in an American lab context and not a Chinese one or elsewhere.

The secret liberalization of animal drugs

Imagine if there were a human regulatory pathway called, say, 'expanded accelerated approval', or XAA. Imagine if the FDA designed this XAA pathway to incentivize development in chronic, serious conditions that are difficult and expensive to run trials for. What might happen if they allowed the use of biomarkers and surrogate endpoints based on an explicitly ‘reasonable’ correlation to clinical endpoints, rather than a supposedly robust correlation, with the restriction that companies would have to run a full clinical trial in five years or their drug would be pulled off the market?

First, way more companies could tackle serious, chronic conditions with a wider variety of approaches. Right now, it costs about $180 million to bring a drug to market for an average condition, even an orphan condition. Serious, chronic conditions cost upwards of $1 billion in development.

This cost barrier doesn’t just limit the companies that can do a trial in conditions like Alzheimer’s to the biggest companies and their partners. It also limits the approaches people are willing to take, as nobody’s willing to risk $1 billion on a therapeutic or modality that will look stupid if it fails. Risking $100 million (or hopefully even just $50 million), although still a lot of money, is much more palatable for the average large VC investor.

Second, patients could have a much wider variety of treatments to choose from, unveiling diversity in the diseases themselves. One of my most firmly held beliefs in biology is that many chronic conditions, such as Alzheimer’s, Parkinson’s, or chronic kidney disease, are actually sets of different conditions with common symptoms. This diversity is hidden, though, because treatments have to target the average patient in order to yield successful trials. Treatments that would be effective for a small subset of patients and ineffective for the majority of patients end up looking mostly ineffective when applied to the entire population.

Real-world evidence of many different types of treatments in many different types of patients could reveal that diversity in a way that massive, expensive, one-off trials don’t. Right now, this is only found accidentally by physicians, who don’t have the resources necessary to explore it. This real-world evidence wouldn’t be a replacement for a pre-registered, randomized controlled trial, but it’d be much more useful than one-off case studies by physicians.

Third, cheap drugs and treatments could become more common. Right now, every treatment, if approved, has to immediately start making back its cost of development. Debt and equity holders demand repayment. Cheaper trials could mean cheaper drugs.

Immediately, our conversation appeared as legible lines of translucent green text, which seemed to be floating in the space between us. “Holy shit,” I said (duly transcribed). He showed me that I could turn off the transcription by tapping twice on the glasses’ right stem, and turn it back on by doing the same again. He added speaker identification by changing a setting on his phone. The restaurant was small and noisy, but the glasses ignored two women talking loudly at a table to my left.

Lavakare’s company is called TranscribeGlass. He has financed it partly with grants and awards that he’s received from Pfizer, the U.S. Department of State and the Indian government, programs at Yale, and pitch competitions, including one he attended recently in New Orleans. His glasses require a Bluetooth connection to an iPhone, which provides the brainpower and the microphone, and they work best with Wi-Fi, although they don’t need it. You can order a pair from the company’s website right now, for three hundred and seventy-seven dollars, plus twenty dollars a month for transcription, which is supplied by a rotating group of providers.

Fake New Yorker Cartoons I generated on o3—